Is It Time To Fix your Variable Rate Mortgage?

November 24, 2016

Rate Update – Who’s Driving The Bus?

January 18, 2017

The Bank of Canada (BOC) kept rates the same this morning, which may seem like a forgone conclusion, however, there was talk over the past couple of weeks that there might be a rate decrease!

Since our last update the mortgage interest rate landscape has completely changed. Take a look at our blog post titled “Is it time to fix your mortgage” to get a better understanding of what’s going on.

Our goal when we write these updates is to give you actionable information, not make you a mortgage expert. However, given recent political events we are getting a lot of questions from clients trying to get a better understanding of why rates are on the rise. Since mortgages are funded by the bond market, I’ve broken it down into a two key points that impact them.

Bonds hate Uncertainty:

Trump is uncertainty personified. Since most of the US debt is held by foreigners, Trump’s shoot from the hip approach has demanded a premium in the market place.

Bonds hate Inflations:

What would you rather have $1 today or $1 five years from now? If you answered five years from now, let us know where we can ship your Trump University degree. If you answered today then you understand the effect of inflation on bonds. Trump’s policies are incredibly inflationary. He wants to reduce the “illegal” work force, bring back more jobs to an economy reaching full capacity AND he wants dump tons of money into the system by building infrastructure. It’s like throwing a match on a pile of kindling that has finally dried out after being waterlogged for 8 years.

What’s next for your mortgage:

Should we lock in for the longest possible term?

No! We always recommend terms no longer than 5 years. Any longer than that and you are paying too much of an interest rate premium.

Are interest rates going to go through the roof?

In the short term we may see more rate increases as the Federal Reserve raises rates later this week, however as mentioned in “Is it time to fix your mortgage” post, a lot of the future has been priced into the market. Given our experience our best guess is that over the next three years a rate of 3.35% for a 5 year fixed mortgage could be the high point.

Should we fix our variable rate mortgage?

It’s complicated. You need to read the “Is it time to fix your mortgage” blog post.

Key Points From The Bank of Canada Announcement

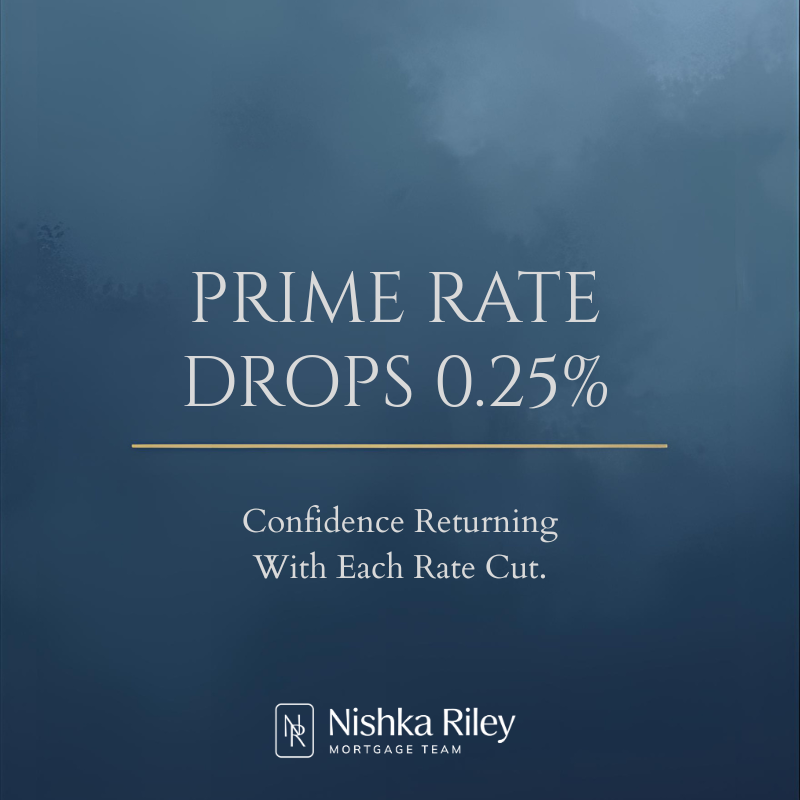

- Prime rate not changed

- US economy starting to reach full capacity

- Canadian economic growth looking better, but…

- Canadian exports continue to disappoint

How Your Mortgage Is Impacted

- Prime rate remains at 2.7%

- Fixed rates have risen by 0.35%

- Banks starting to tier pricing depending on home use

- Variable mortgage rates expected to stay the same until mid 2018

- Rate holds for purchases or maturities now available until April 2017

Give me a call! We can discuss how your current financial situation fits into today’s economic environment, how the right mortgage strategy could save you thousands of dollars over the term of your mortgage and how to maximize the value of your home in today’s market.

The next Bank of Canada meeting is January 18th, 2017.

Don’t forget to Like my Facebook Page to keep current on news in the real estate market!

{kind=link}

{kind=link}

{kind=link}