Rate Update: If Not Now, Then When?

July 30, 2025

Rate Update: No Tricks, Just Treats

October 29, 2025

September 17, 2025

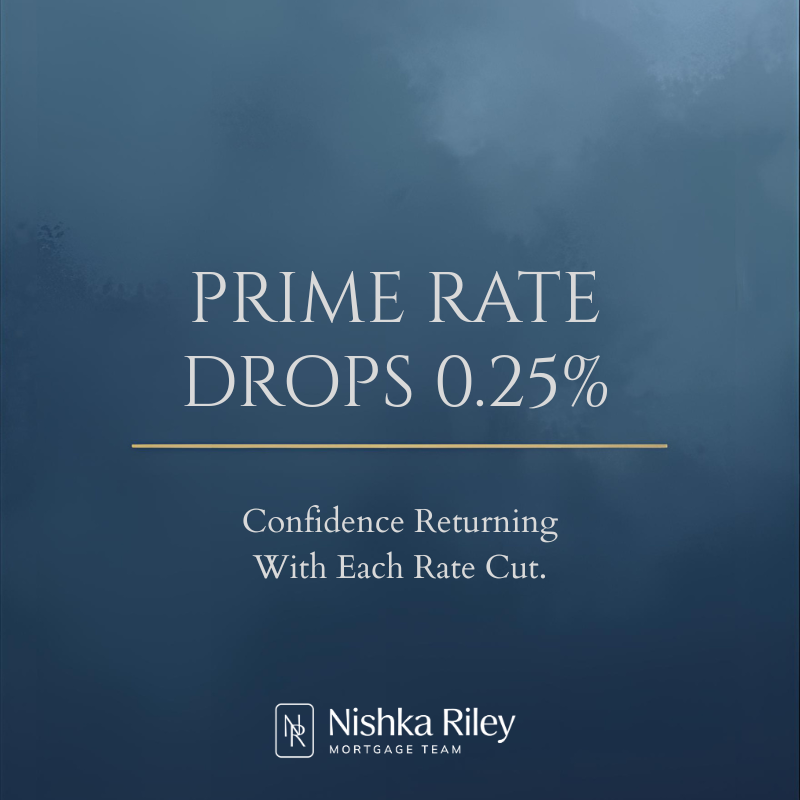

Governor Tiff Macklem dropped the Bank of Canada rate today by 0.25%, which now means the prime rate is 4.7% at the major Canadian banks. While the move didn’t come as a complete surprise, it wasn’t exactly something most people thought was in the cards for 2025.

So the question is: what changed?

Here’s a quick summary of the highlights from the Bank of Canada meeting—and more importantly, what it all means for real estate in North Vancouver and the Vancouver area in general.

What’s Going On Economically

First, let’s look south.

Inflation in the U.S. is still persistent, but not out of control. The tariffs are being passed through to consumers and impacting their inflation numbers, but at some point, this will become part of the regular cost of living.

Here in Canada, inflation has cooled to a level that gives the Bank of Canada breathing room.

Another shift is happening in the bond market.

Five-year Government of Canada yields are dropping, which usually signals that the market expects more rate cuts—or at least no sudden increases. At the same time, the U.S. Federal Reserve has cut its prime rate today, also by 0.25%, with one or two more cuts likely before the year wraps up.

On our side of the border, GDP did contract recently, but much of that looks like a timing issue. The U.S. loaded up on Canadian goods before tariffs kicked in, so the pullback in exports may not be a long-term trend. Still, there’s no question that consumers here are slowing down. Job numbers are weaker, population growth is tapering, and household spending is softening. All of this points to a slightly weaker economy—exactly the kind of backdrop that allows the Bank of Canada to keep easing.

North Vancouver Real Estate: Where Things Stand

Closer to home, we’re starting to see a more balanced conversation between buyers and sellers. Prices are down about 2% since the start of the year and roughly 1% in August alone. Sellers are adjusting, and buyers are responding.

Detached home sales jumped 13% compared to last August, and townhouse sales climbed just over 10%. Condo sales slipped a little, but the overall trend is clear: transaction volumes are rising. At the same time, new listings are coming in at about their ten-year average. That means supply still feels healthy for now, but if sales keep pushing higher, today’s “plentiful” inventory could tighten up quickly, which could lead to home prices increasing.

What we are seeing: Over the past 2 weeks, I’ve seen a significant increase in new mortgage inquiries. The prospect of lower borrowing costs is creating confidence in First Time and move up buyers to take action. Combine this with the significant value that real estate in North Vancouver represents at the moment, and you have a recipe for this potentially being a turning point in real estate prices.

Where Mortgage Rates Seem Headed

So what’s next?

With five-year bond yields drifting down, there’s room for fixed mortgage rates to ease further. The Bank of Canada has made it clear they’re open to another cut if needed, and most observers are betting we’ll see at least one more by year-end. The U.S. is cutting too, which only reinforces the direction of rates.

For buyers, our message is clear: don’t tie your decision to purchase a home with waiting for rates to drop. With each rate drop, consumer confidence grows, and so does your competition. If you are a move up buyer, the window is closing on your ability to write an offer with subject to sale.

Bottom Line

The Bank of Canada’s latest move wasn’t just about rates—it was about opening a door.

Inflation in Canada is under control, bond yields are sliding, and the Fed is easing too. All signs point to at least one more cut in 2025.

In Vancouver, sales are picking up, prices have softened, and inventory is still available—but that won’t last if current trends continue.

For buyers, this is the moment to take advantage of choice in the market before the balance tilts back toward sellers.

If you’ve been waiting, now might be the time to act.

If you’re selling, realistic pricing today could put you in front of a wave of renewed demand tomorrow.

Final Thoughts:

I know this update took a slightly different path—I wanted to highlight the real opportunity showing up in today’s real estate market.

..and I’ll leave you with this:

If you’re a first time buyer you’re probably wondering if you’re ready and how your’re going to make a mortgage fit into your budget.

If you’re a move up buyer you’re probably feeling overwhelmed with how to make the jump from one home to another.

To both of you I say this: I’ve been here close to 4,000 times now, and I know the way! And what I mean by that is I’ve close to a thousand people, just like yourself, through the stress, the uncertainty, and the emotions of making a big move…in addition to the financial aspect of it all.

Reach out to me. If you’re my client you know how much I enjoy figuring out the “next step”. If you’ve come to this post on the search of a mortgage broker, click on over to my reviews. You can see that I’m approachable – and don’t bite 😉

What I’m trying to convey is you’ll be surprised the clarity a 20 minute conversation will give you. I guarantee that after our call, you’ll know what the right move is for you.

Thanks for stopping by!

The next Bank of Canada meeting is October 29th, 2025

Did you Like this post? Follow me on Instagram or Facebook! My feed is filled with current news and where I share my ideas on how to get where you want to go in real estate.

{kind=link}

{kind=link}

{kind=link}